Singtel is well-liked by many investors. However, it has not been a great year investing in Singtel when it is down about 14%. Singtel is my first investment in 2018 and I have been holding it since then and it is not making any returns for me except the 5.6% dividend yield. To be honest, buying Singtel is a mistake because I did not study the industry Singtel is in and why Singtel share price is dropping. There is always a reason why its share price drops. I guess I have paid the price for not doing any substantial research. I am staying cool with Singtel because I think that the 17.5 cents dividend will be sustainable for the next two years.

What is Singtel

We all know the brand Singtel, the largest telco in Singapore with more than 4 million customers or close to 50% market share but Singtel is more than just Singtel. According to its factsheet, Singtel prides itself as the leading communications group with operations and investments around the world. 75% of Singtel’s underlying net profit comes from operation outside Singapore. Singtel, as a group, serves 717 million customers worldwide including India (40% interest in Bharti Airtel #2 Telco), Indonesia (35% interest in Telkomsel #1 Telco), Philippines (47% interest in Globe #1 Telco), Thailand (23% interest in AIS #1 Telco) and Australia (100% interest in Optus #2 Telco). These operations and investments form the Group Consumer segment. There are two other segments under Singtel Group which are Group Enterprise and Group Digital Life. Group Enterprise can be described as offering governments and companies solutions that cover mobile, voice and data infrastructure, managed services, cloud computing, cyber security (Trustwave), IT services (NCS) and professional consulting. Group Digital Life focuses on digital marketing (Amobee), regional video services (HOOQ) and data analytics (DataSpark).

Singtel Group has made improvement for the past 4 financial years to be less reliant on its telco business. In FY14, 86% of its revenue comes from traditional carriage which includes Group Consumer and Group Enterprise excluding ICT and now it is down to just 76%. Digital Business or also known as Group Digital Life (Amobee, HOOQ, DataSpark) and ICT (NCS and Trustwave) now contributes 6% and 18% to total group revenue in FY18.

Group Consumer

In Group Consumer, Singtel Group owns the second largest telco in Australia – Optus. Singtel Group also own 40% of Bharti Airtel (second largest telco in India), 23% in AIS (largest telco in Telco), 21% of Intouch, 47% of Globe (largest telco in Philippines) and 35% of Telkomsel (largest telco in Indonesia).

Despite strong competition from MVNOs in Singapore, Singtel managed to increase its net add for postpaid customers by 41000 in the latest quarter result. This is the highest Singtel net add for postpaid customers in the past year. However, the increase in postpaid customers did not increase the mobile revenue significantly. This resulted in postpaid ARPU to decrease by 11%. Singtel blame the fall in ARPU because of the decline in local & roaming voice usage and dilutive impact of SIM-only and mobile share plans. In my opinion, postpaid net add amount is not as important as ARPU for postpaid. Having positive net add means that Singtel is still the preferred telco among people living in Singapore but a decrease in ARPU is a worry sign for investors. This means that the increase in revenue cannot keep up with the increase in net adds for postpaid customers.

Singapore Telco Industry

Singapore currently has 8 telco operators – Singtel, StarHub, M1, Circles.Life, Zero 1, Zero Mobile, MyRepublic with TPG Telecom coming onboard next year as our fourth telco.

Source: Annual Report of StarHub and M1 and CIMB Analyst Report

Singapore telco industry market size has been contracting since 2015. It is expected to contract further when TPG Telecom comes onboard next year. As mentioned earlier that Singapore has 8 telco players, everyone is sharing a smaller pie, it is quite depressing to see how the industry has evolved into as an investor perspective.

In late 2016, IMDA awarded TPG Telecom the license to be the fourth operator in Singapore. Sentiment in Telecommunication sector is mixed for many analysts. There is one analyst who is quite optimistic about the sector said that the capital expenditure for TPG Telecom in Singapore is not enough to shake up the whole industry. DBS Analyst in his report states that the capex of $66 million spent on infrastructure is much lesser than what was planned. He also cited how Reliance Jio, which offers extremely cheap telco plans for the Indian market, spent more than US $20 billion to build its infrastructure to compete existing players such as Bharti Airtel. As TPG Telecom is building its infrastructure from ground zero, we do not know how its network quality will be when it starts service next year.

For TPG Telecom to snatch market size from existing players, it would require them to start from the price sensitive customers. Therefore, Singtel, StarHub and M1 started partnering with MVNOs to prepare themselves from the impending arrival of TPG Telecom. (The) Boring Investor wrote great articles which I will share it with all of you here. In the past, I would have thought why will Singtel, StarHub and M1 partner with MVNOs when MVNOs are offering much better plans than the former. For example, Singtel view MVNO as an important part of its mobile network strategy and MVNOs serve different segments of the market which Singtel may not able to target. Singtel as a wholesale partner will see incremental revenue with more MVNOs coming on board. In my opinion, from the perspective of a consumer, it would be tough for me to jump ship to TPG Telecom if it is offering cheaper plans than MVNOs or my current SIM Only plan with Singtel. I am with Singtel mobile for close to 4 years, I am satisfied with the quality of Singtel’s 4G network. TPG Telecom as a new operator would not be able to meet the standard of what Singtel infrastructure is having when it starts operating next year. Customers on MVNOs’ plan who understand that MVNOs are riding existing telco infrastructure which are definitely better than TPG infrastructure, might think twice jumping ship to TPG Telecom. I might be wrong, but I do not think TPG will disrupt the industry as bad as what Reliance Jio did to India.

For TPG Telecom, it has to meet few requirements set by IMDA such as 95% coverage at street level by 1 Jan 2019, 85% coverage at In-Building by 1 Jan 2020 and 99% coverage at MRT Underground Stations & Lines. DBS Analyst also wrote the consequences of failure to meet IMDA requirements such as fine, forced consolidation, dispose spectrum assets to incumbents. As of Sep 2018 conference call by TPG, it covers more than 90% of outdoor areas in Singapore and is on track to meet the first IMDA requirement by 1 Jan 2019.

Australia Telco Industry

Telcos in Australia had a much intense competition due to the impending arrival of TPG Telecom in Australia as the fourth operator. However, there was some relief after TPG Telecom agreed to merger of equal with Vodafone Hutchison Australia. It is a win-win situation for every telecom operator in Australia as it means less competition. However, with the merger, it would also mean that TPG Telecom have more resources to fight with the existing telco operators. We shall have a wait and see attitude for the impact of the merger in the coming quarters.

Regional Associates

Regional Associates or the investments made by Singtel are very important to Singtel’s result. 2018 is a tough year for Singtel as we could see a significant drop in Telkomsel and Airtel earnings which are the main contributors for Regional Associates.

Telkomsel

Telkomsel’s contribution to Singtel earnings has been declining for a few quarters. With significant rate of decline in recent quarters. The reason was due to price war for the registration of SIM cards for prepaid cards. Since the registration for SIM card is over, Telkomsel started to raise its charges once again. This resulted in 24% increase in net income for its latest quarter. Hopefully this momentum will continue for Telkomsel in the coming quarters!

Singtel’s comment on Telkomsel

“Yes, with regard to Indonesia I think there is still a bit of industry repair coming through this quarter where we see prices have been lifted up across the board and I think recently all the telcos have actually reported their results. I think it’s a healthy trend. With regard to how Telkomsel fits in the marketplace, whether it looks at market share and profitable growth definitely we have to balance the two. It’s important to grow profitable share but at the same time there are regions where we can see that there is a lot more intense competition and, in those areas, Telkomsel will want to make sure that it protects its scale advantage and competes aggressively in those regions. On the whole, in the overall strategy we do think that the industry can go back to a healthier growth by everyone pricing more rationally and lifting price up across the board, which we have seen in the July period post the Lebaran period and we continue to see that healthy move going into the last quarter of the calendar year. In general, I think I would say as a market leader in Indonesia, Telkomsel want to continue to defend its position and make sure that it has cost and scale advantage but at the same time price rationally to ensure that the overall market can grow healthily.

– Yuen Kuan Moon

Bharti Airtel

It is depressing to write about Bharti Airtel’s contribution to Singtel’s earnings. Ever since Reliance Jio came to the scene in 2016, it has been a tough fight for existing players. It resulted in many rounds of consolidation to just three main players now but there isn’t much relief to earnings. Bharti Airtel contribution to Singtel’s earning is -$176 million in Q2 earnings. The bright spot for Bharti Airtel would be its African business where it has double digit growth. Recently, Singtel invested US$250 million in Bharti Airtel Africa pre-IPO funding. I feel that this is a great investment made by Singtel as there is still room to grow for Bharti Airtel African business. According to Singtel, The African continent is projected to be the world’s second-fastest growing economic zone and the fastest growing mobile market with unique mobile subscribers expected to increase from 420 million at the end of 2016 to more than half a billion by 2020.

AIS

There are three players in Thailand – Advanced Info Service which Singtel has 23% stake, True Corporations and Total Access Communications. The mobile industry in Thailand is expected to grow low to mid-single digit due to increase demand in data usage. There is no new entrant coming onboard so competition is within the existing players.

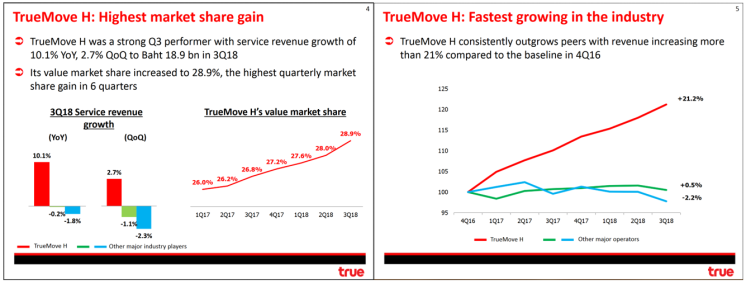

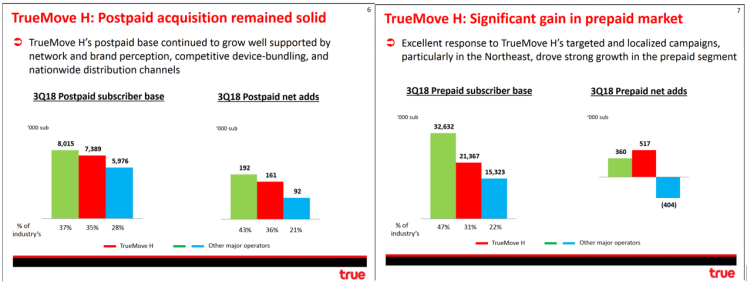

TrueMove has been aggressive in subscribers net adds. TrueMove was once the third largest telco in Thailand and has since moved up to be the second largest telco. TrueMove market share has been increasing from 26% to the current 28.9% in just 7 quarters.

In terms of postpaid subscriber base, TrueMove is catching up with AIS numbers and might soon overtake AIS to be the telco with most postpaid subscriber base. This is so for the prepaid segments where TrueMove recorded more net adds than AIS.

“I think in Thailand it’s the case where we are facing a very aggressive player who has gone from a number three position to a number two position and having got to a number two position continues to accelerate and is doing things like packaging free prepaid handsets with their service. I think from our perspective at AIS I think it’s important to look at our scale and to make sure that our number one position is not compromised. Moving on to the balance between profitability, I think this is something that we look at very seriously in AIS and I think one of the key things that we look is to make sure that people who threaten the AIS number one position will understand that there is a line in the sand that we will draw and that we will respond. At the same time, to ensure that we preserve our profitability and our margins we will also take a look at making sure that our cost structure is right as well. I think it’s talked very clearly about where it’s focusing on and the high value postpaid segment and that they will be responding in the prepaid segment on a regional by regional basis, geographic region by geographic region basis rather than across the board. Let’s see how that plays out but at the end of the day it’s a very clear line in the sand that we have drawn and that we are set to respond to some of these threats to our leadership position while maintaining or profitability.”

– Allen Lew

Competition is not as brutal as the one at India. AIS is still able to increase its revenue. However, the rate of increase in revenue cannot keep up in the rate of increase in expenses. Therefore, even though revenue increase for AIS, net profit dropped slightly. The focus for AIS should be to look into cutting costs so that it can still contribute positively to Singtel’s earnings.

Globe Telecom

In my opinion, I am least worried about Globe Telecom. Recently, Philippines just announced that Mislatel consortium led by China Telecommunications Corporation (China Telecom) among others to be the third telco in Philippines competing with Globe and Smart. Mislatel consortium will be able to accept subscribers from 2019 onwards.

Why am I least worried about Globe Telecom? These are few reasons.

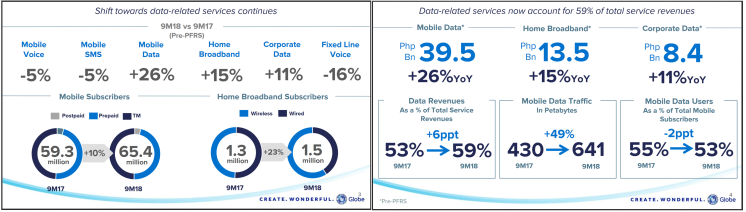

Globe Telecom is shifting its focus to data-related services. The figures from their latest earnings are pretty. Mobile data and corporate data up 26% and 11% YOY and data-related services now account for 59% of total service revenues. Globe subscribers net adds are healthy too where it is up 10% YOY.

Globe Telecom is not just a telco but also into Financial Services and Telehealth. Globe invested 45% in Mynt which addresses financial inclusion through mobile money, micro-loans and technology. There is definitely room for growth for Globe and Mynt when 70% of the citizens do not have a bank account to save money. It is difficult for citizens to take a loan as 90% of them do not have a credit score. As a result, the interest rate charged by informal lenders is as high as 20%. So Mynt is launched to bridge this gap.

When there are just 54% licensed physicians who are active and that there are only 3.5 doctors for every 10000 patients, Telehealth is what I call a value-added service. How Telehealth works is that subscribers can call anytime and anywhere in the country and a licensed doctor will be assisting the caller for any healthcare advice. I think this is one of the best telco I have ever seen…

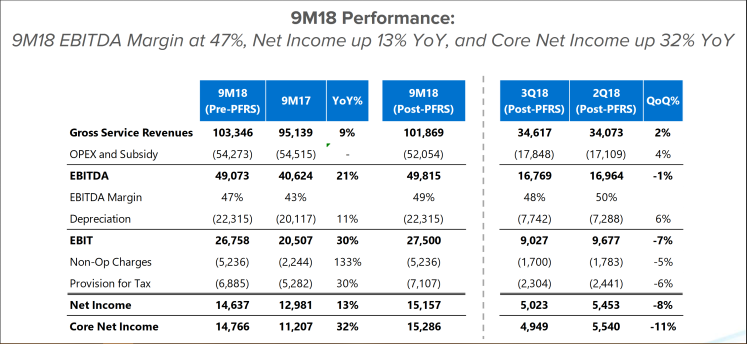

When it comes to cost management, Globe Telecom would be the best out of all telco Singtel has invested in. Comparing YOY figures, its revenue service went up by 9% but its operating expenditure and subsidy was stable. This resulted in its EBITDA margin to inch up 4%. Overall, its core net income went up by 32% YOY. I have faith in Globe Telecom’s business and the other business ventures that Globe are in. 2019 onwards will be a tough year for Globe Telecom since China Telecom led consortium will be accepting subscribers so we shall see how Globe will perform when the third telco comes in.

Group Enterprise

In general, Group Enterprise revenue consists of ICT and Carriage. ICT refers to revenue from managed services and business solutions. Cyber security, facility management, managed and network services, and value-added reselling and services form the managed services. Carriage revenue comes from Data and Internet, mobile service, sale of equipment, fixed voice and TV and digital business revenue.

The focus of this article is to analyse their ICT business which Singtel describes it as its growth engine. Since it is being described as a growth engine, I as an investor would have expected the revenue or EBITDA to increase by double digit. This is not for Singtel cyber security business in the latest quarter! Global Cyber Security business revenue which comprises of Managed Security & Tech Services and Payment Card and Industry Compliance were down by 2% YOY for the latest quarter and down by 2% YOY. Managed Security & Tech Services was up 6% YOY but it was impacted by Payment Card Industry Compliance where it declined 35%. Singtel explains the lacklustre result that its cyber security business was impacted by lower sales in USA due to commoditisation in the traditional PCI compliance business. However, cyber security business in Asia Pacific region growth is higher than the market growth of 8.62% estimated by Gartner.

In other news, Singtel consolidated its cyber security capabilities, technologies and resources of Singtel, Optus, Trustwave and NCS, under the Trustwave brand. You can refer to its news release here . There are few benefits for the integration such as Broader security services portfolio, Increased focus on industry-leading technologies, More cyber security resources and talent, Advanced security training and continued education and Separate business unit focused on compliance. We shall see how the new Trustwave will contribute positively in the coming years.

ICT excluding cyber security business revenue was not below expectations because Singtel completed large projects a year ago and did not have similar size projects this year. There was a halt in government IT projects after the cyber attack that happened to SingHealth so the government had to do necessary checks before continuing the project. As a result, Singtel only received new contracts late in the quarter. Singtel stressed that order book remains strong and the ICT business will be expected to grow in the second half of FY19.

In summary, the guidance for Group Enterprise was cut from growing low teens to growing high single digit mainly due to the commoditisation in the traditional PCI compliance business. Singtel is optimistic that despite the cyber attack that happened to SingHealth, the Government is still committed to its smart nation plans. So, with this commitment, Singtel will have more opportunities to work with the Government to allow businesses to go digital.

Group Digital Life

Group Digital Life (GDL) consits of businesses in Amobee, HOOQ and DataSpark. 98% of GDL’s revenues come from Amobee while the remaining come from HOOQ and DataSpark. GDL has not been profitable since the group first established a few years back.

Amobee is a wholly-owned digital marketing company of Singtel. Singtel has poured over $1 billion dollar into Amobee since its acquisition in 2012. For example, Singtel acquired adconion – true cross channel advertising for US$240 million, Kontrea – real time brand intelligence for US$150 million and Turn – integrated data, analytics and activation platform for US$310 million. Recently, it acquired Videology for about US$101 million. With all the acquisition, Singtel would want to build up Amobee’s technological edge to make Amobee one of the world’s top leading independent digital marketing players.

Is 17.5 cents dividend sustainable?

This is the most important question that all Singtel’s investor is asking. Is the 17.5 cents dividend sustainable? In the past, Singtel would guide its dividend payout ratio to be 60%-75%. This is well within reach in the past. Every year, Singtel will distribute about $2.86 billion dividends to its shareholders. In FY18, Singtel distributed 81% of its underlying net profit as dividends. That’s way above the 75% max payout ratio. From FY2018/2019 to FY2019/2020, dividends will be maintained at a flat rate of 17.5 cents (no change to the amount). Can the 17.5 cents dividend be sustained for the next two years? Singtel thinks that it is confident to maintain the 17.5 cents dividend despite the bad earnings from Bharti Airtel. The Group’s FCF for FY2018 is $3.6 billion which is higher than the dividend payout of $2.86 billion every year.

“Okay let me just quickly take the dividend question. You would have noticed that for this year we have exceeded our dividend payout. For a large part of it is due to weakness in the associate earnings, particularly Bharti. In the short term we expect pricing pressures in India to continue. So, you know that may adversely impact the profit contributions that we would equity account for Bharti. But as you are aware, Bharti’s dividend payout is relatively low. So, it’s a slight impact on our cash. It will not impact our cash flow significantly. Therefore, our ability to maintain the current dividend of 17.5 cents. So, we thought that it’s important to provide that clarity. ”

– Chua Sock Koong

What’s next after 2020. Will Singtel’s cut its dividend? Singtel will revert its payout to 60%-75% of retained earnings after 2020. We are not sure whether Singtel’s growth engines will outpace the decline in Group Consumer revenue but I think Singtel might be too optimistic about its business outlook after 2020. We shall enjoy the stable 17.5 cents dividend for the next two years and see how the earnings will be like in the future.

Conclusion

It took me more than 3 days to write this article. This is the longest I have ever taken for any post. I cannot think of any other reasons besides geographical diversification why one should buy Singtel. Geographical Diversification – Singtel has operations and businesses not only in Singapore but in other countries. Yes, it is great to have diversification in other countries but not when there are competition in other countries too. Look at India where Bharti Airtel is facing intense competition with Reliance Jio and for the first time in 2018, Bharti Airtel contributed negatively to Singtel earnings. When do not know when will Reliance Jio end this market share snatching with the existing telcos but it seems that it will not end in the next few quarters. In Philippines, Globe Telecom is going to face competition as the third player backed by China Telecom is entering the industry next year. In Thailand, the second telco largest player is aggressive in becoming the market leader of the industry. AIS has to defend its market leader position and you know the typical move that business will do – cut prices, hurting investors. When you have business all over the world, what company will face is currency risk. Singtel’s associate earnings would perform slightly better if the exchange rates such as Indonesia Rupiah and Indian Rupee appreciated against SGD.

Currently, growth in ICT segments and GDL is below my expectation. Singtel mentioned that ICT revenue should grow in the second half of the year and I hope that the consolidation of all resources into one Trustwave will grow the segment at a much faster rate. We shall see in the coming quarters.

Let’s be honest – Singtel is not a growth company. Singtel is just a cash-rich generating company. The growth in ICT segments and GDL in my opinion is just to cushion the declining revenue in Group Consumer including its regional associates. At 5.6% dividend yield, I would rather buy into growing REITS such as Mapletree Logistics Trust which is expected to distribute more in the coming years.

It is a grave mistake for me to invest in Singtel, let’s move on. Unless Singtel can prove me wrong that its growth engine can outpace the decline in Group Consumer then will I consider averaging down. If not the funds that are meant for averaging down Singtel will be used for other purposes.

Hi,

What are your views on the recent Singtel partnership with Geneco to enter the electricity retailer market as SingTel Power? Is it a good strategy to retain existing customer base with carrots and perks and at the same time having another revenue stream?

LikeLike

Hi CuriousCat, in my opinion, I feel that is a good strategy to retain or attract customers to sign up plans with Singtel. As for creating another revenue stream, we need to wait for the following result quarter to see. I think that positive impact to earnings will be minimal.

LikeLike

Like!! Great article post.Really thank you! Really Cool.

LikeLike

Like!! Great article post.Really thank you! Really Cool.

LikeLike