In this article, I will be analysing two of the largest Industrial REITS – Ascendas REIT (AREIT) and Mapletree Industrial Reit for the second time. You can refer to the first analysis that was posted in 2019. The format for analysis remains the same.

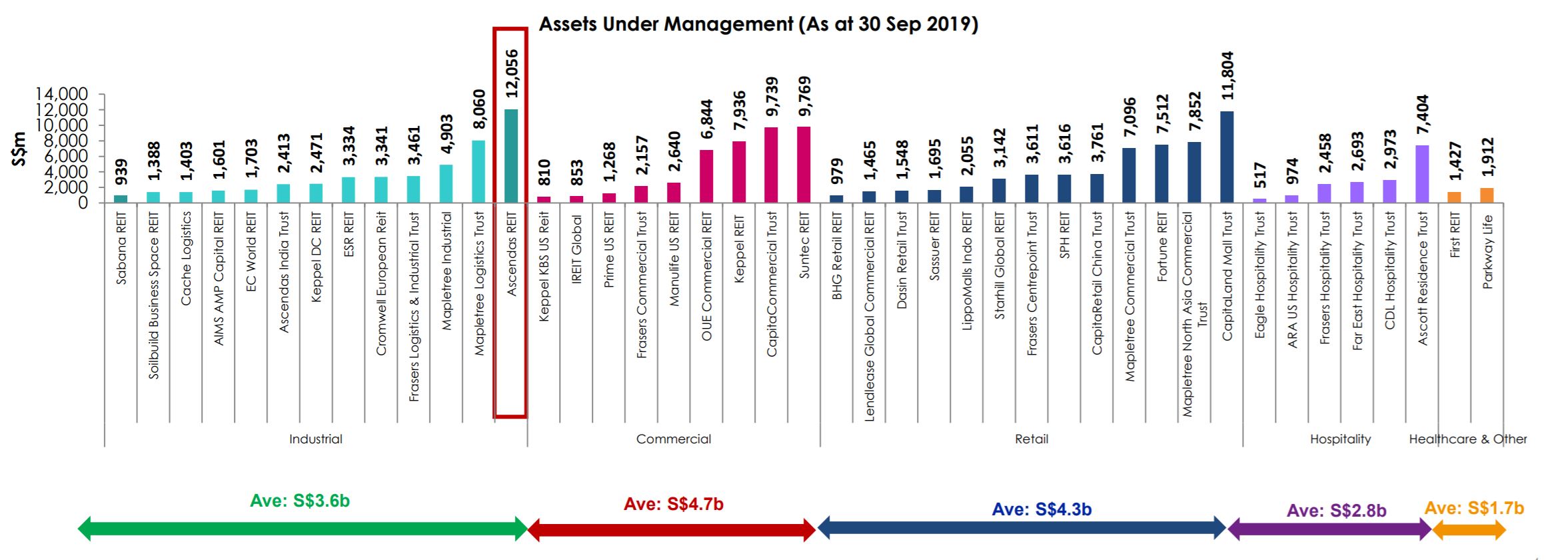

AREIT did a comparison of all REITS’ Assets under Management (AUM) chart. AREIT is the largest industrial REIT with more than $12 billion AUM. MIT is the third largest industrial REIT with $4.9 billion of assets.

Both AREIT and MIT have strong sponsors. Ascendas Singbridge, a joint venture by both Temasek (51%) and JTC (49%), owns 19% of AREIT is a leading sustainable urban development and business space solutions provider. Ascendas Singbridge is a subsidiary of Capitaland after the $11 billion acquisition of Ascendas Singbridge to create Asia’s largest diversified real estate group. On the other hand, Mapletree Investments Pte Ltd is the sponsor for Mapletree REITS. Mapletree Investments was established in 2000 after Port of Singapore Authority (PSA) transferred non-port properties to Temasek.

Both REITS have been growing since its listing. AREIT was listed in 2002 and its DPU grew 4.8% CAGR. Even though MIT is late to the game, it also experienced gain in DPU every financial year. From 8.41c DPU in FY11/12, MIT grew its DPU by close to 40% to 12.16c DPU in FY18/19.

As usual, I will analyse the portfolio, financial health and the industry outlook of both REITs.

Portfolio Overview

AREIT has 200 properties in Singapore, Australia, United States and United Kingdom as at 31 December 2019. Singapore’s properties are categorised into 5 sections – Business and Science Park, Integrated Development Amenities and Retail, Hi-Specs Industrial, Light Industrial and Logistics. Australia’s properties can be categorised into 2 sections – Logistics and Suburban Offices while its United Kingdom properties are logistics. Recently, it acquired 28 Business Parks in the United States.

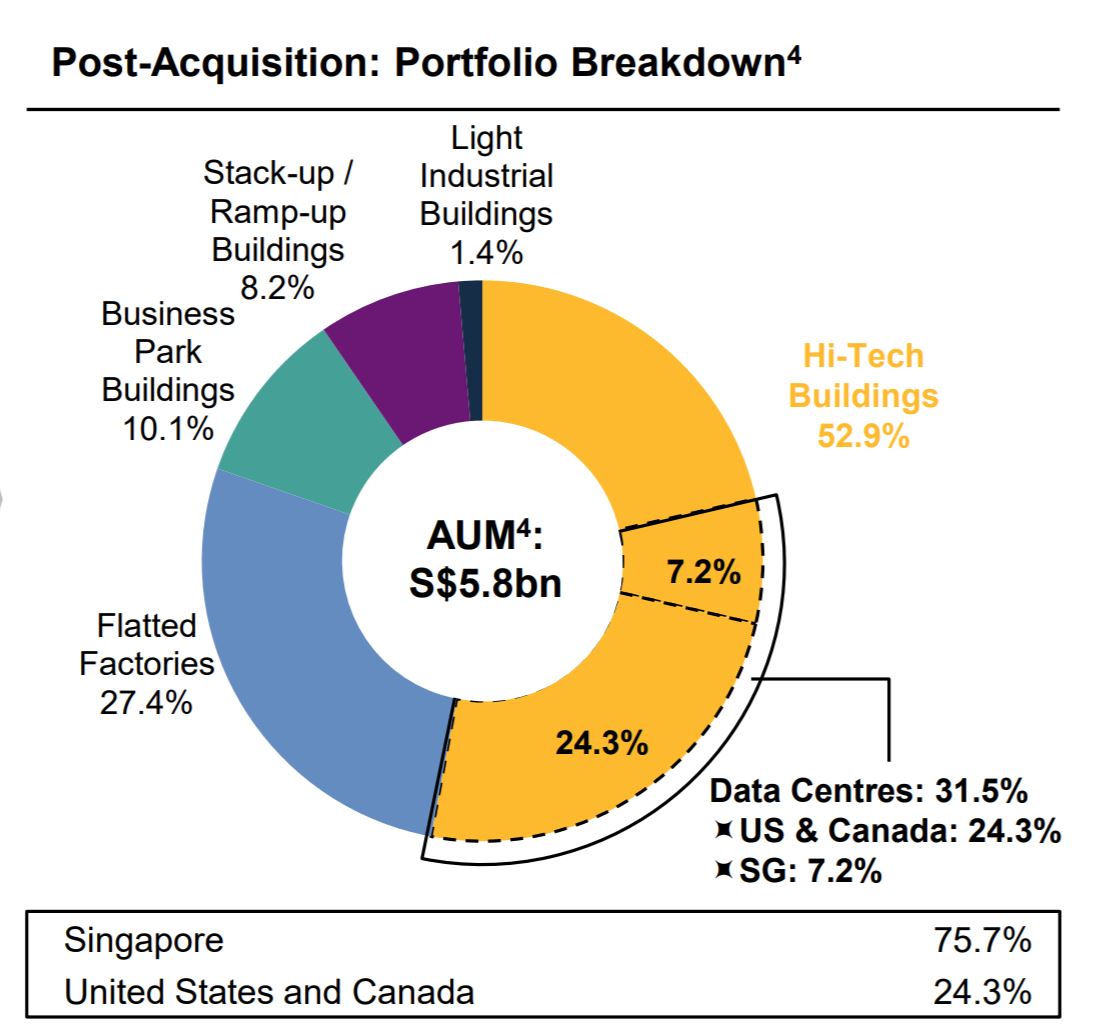

MIT has about 104 properties including the recent acquisition of 27 US and Canada Data Centres in 2018 and 2019. MIT’S Singapore properties are categorised into 5 sections – Hi-Tech buildings, Business Park buildings, Stack-up/Ramp-up Buildings, Flatted Factories and Light Industrial Buildings.

AREIT occupancy rate in Singapore stands at 87.2% while MIT’s figure is at 90.5%. AREIT occupancy rate in Singapore is relatively stable, hovering around 87-88% for the past three quarters. On the other hand, MIT sees its occupancy rate increased slightly for the latest two quarters.

Occupancy rate for both AREIT and MIT’s overseas expansion is stable. There is nothing much to discuss since it is still quite resilient. However, the focus should be more of the Singapore properties where 72% and 82% of AREIT and MIT properties are in.

AREIT also provided a chart that compares its occupancy rate with the industrial average. However, to my surprise, AREIT occupancy rate is lower than industrial average across the board except Logistics properties.

Comparing similar categories between AREIT and MIT, we can get insights that MIT figures are nicer. Occupancy rate of 85.1% for MIT’s Business Science Park is better than the one at AREIT’s at 83.8%. However, both REITS occupancy rate is lower than the industry average of 86.2%. Next, occupancy rate of 85.6% for AREIT’s Light Industrial Building is better than the one at MIT’s 81%. However, both REITS occupancy rate is lower than the industry average of 87.5%. MIT did well in the Hi-Specs Industrial sector where its occupancy rate stands at 98.4%, way better than the industry average of 87.5% and AREIT’s occupancy rate of 85.7%.

Only looking at statistics from FY19/20 to FY21/22, we could see that expiring leases by gross rental income is lower for MIT. Take for example, only 2% of leases will expire for MIT in FY19/20 while 19.4% of leases will expire for AREIT in the same period. In summary, 58.5% of leases in AREIT will expire by FY21/22 compared to 40.4% in MIT. If given a choice between AREITT and MIT based on expiring leases, I would choose MIT. This is because there are fewer leases that are going to expire in the next four years compared to AREIT thus making MIT more stable. WALE for Singapore Properties for both REITS where the majority of its properties are situated is 3.5 years. Overall, both REITS’ WALE stands at 3.9 years. I am a fan of higher WALE as having higher WALE means that the management does not need to find tenants thus providing stability in rental income. However, the con of having a longer WALE is that if the REIT will miss out any opportunity of rising market rental rates unless there are rental review in the lease.

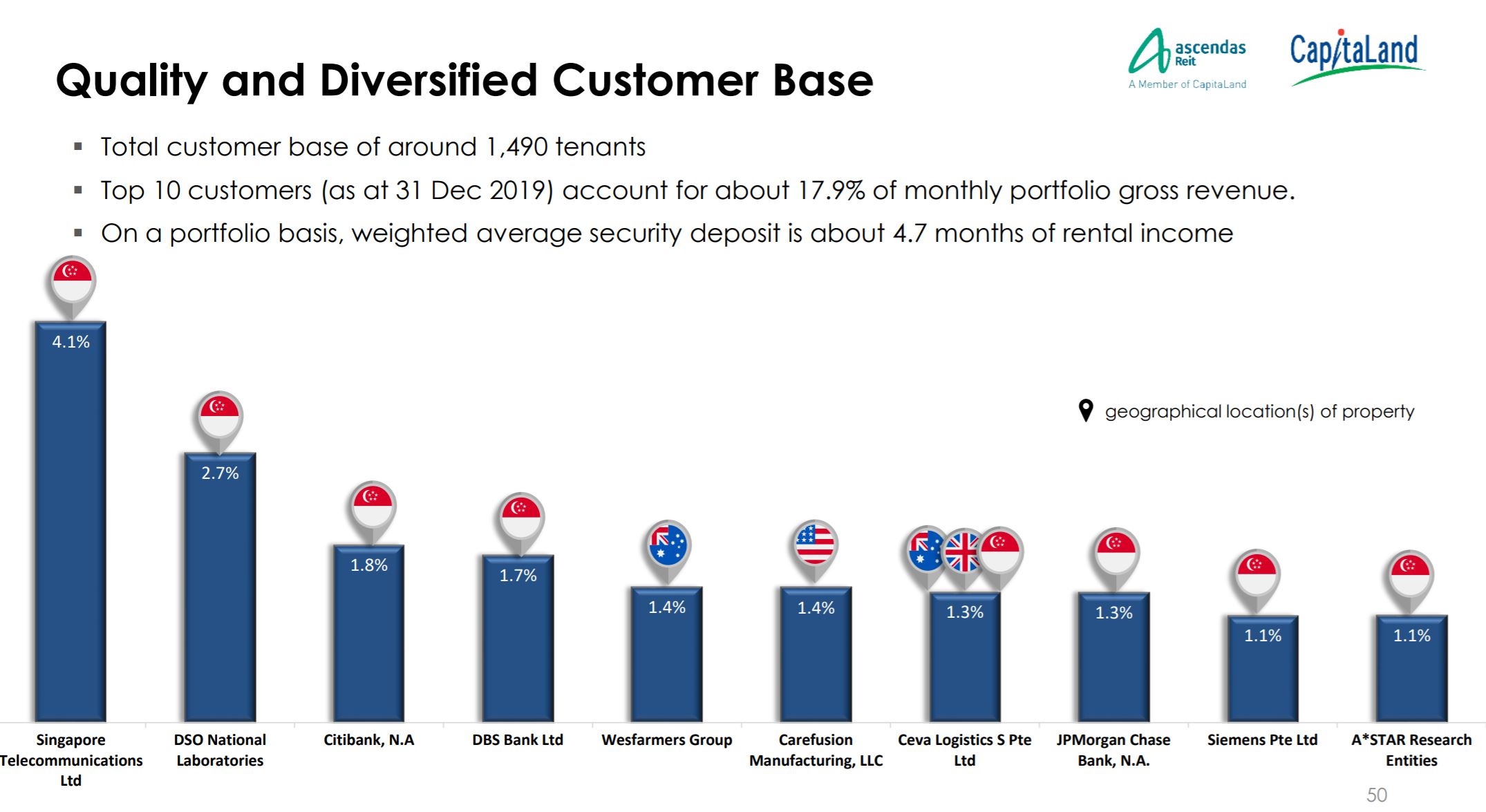

MIT has over 2200 tenants while AREIT has about 1490 tenants. Even if MIT has more tenants than AREIT, MIT top tenant – HP is contributing 8.4% of gross rental income. This means that MIT has key tenant risk. On the other hand, AREIT top tenant – Singtel contributes 4.1% of gross rental income. Due to the high contribution rate at MIT, Top 10 MIT tenants form 28.5% of Portfolio’s Gross Rental Income while the number is just 17.9% for AREIT.

Debt

In this section, we will take a look at the financial health of the REITs. Debt is very important for REITS and investors as this is one of the few methods that REITS finance to acquire properties. We will look into the Gearing Ratio and Interest Coverage Ratio. Before that, we shall look into the credit ratings of both REITS. MIT is rated by Fitch Ratings to have BBB+ with stable outlook while Moody rated AREIT A3.

Gearing Ratio of AREIT is at 35.1% while MIT is at 34.1%. A lower gearing ratio will be preferred in this case. As for Interest Coverage Ratio, MIT has higher figure at 6.8x while AREIT is at 5.1x. Interest Coverage Ratio means how much times its EBIT can cover the Interest Expense. It also determines how easily a company can pay interest on its outstanding debts. Therefore, a higher Interest Coverage Ratio will be preferred. To add on, both REITS have more than 64% of their debt on fixed rates. AREIT has a higher percentage of fixed rates at about 76% while the figure at MIT is 64%. In this zero interest rate environment, it will be wise to select REITS that have lower percentages of debts on fixed rates.

Closing Thoughts

This is the second time analysing both REITS. I revisited both REITS one year later and realised that MIT performance has improved tremendously.

Take for example, MIT’s occupancy rate in Singapore has improved from 87.8% in 2018 to the current 90.5%. On the other hand, AREIT’s occupancy rate stays stable at 87%. Previously in Singapore’s industrial occupancy by sector, AREIT figures are nicer looking than MIT figures. Fast forward to today, tables have turned. MIT occupancy rates are better compared to the 2018 numbers. For example, Business Science Park which contributes 32% of AREIT’s AUM has an occupancy rate of 85.1%, this is only a slight improvement of 84.4% in 2018. Business Science Park which contributes 10.9% of MIT’s AUM has an occupancy rate of 85.1%, a significant improvement from 79.6% recorded in 2018. In addition, Hi-Tech Buildings which contribute close to 31% of MIT’s AUM has its occupancy rate improved tremendously from 84.4% to 98.4%. Looking at expiring leases, overall WALE for MIT has improved from 3.7 years to 3.9 years and only 40.4% leases expire in the next three years compared to 69% when it was analysed in 2019.

MIT also sees its balance sheet improve compared to a year ago. Its gearing ratio improved slightly from 35.1% to 34.1%. What’s more amazing is that it has reduced its fixed debt percentage from 78% to 64%! MIT continued to have a better Interest Coverage Ratio than AREIT at 6.8x which is an improvement from the 6.4x in 2018. On the other hand, AREIT Interest Coverage Ratio continued to slide to 5.1x from 5.3x compared to a year ago.

As I have limited cash to buy, I would now choose MIT over AREIT as first its performance improved tremendously and it has now ventured into owning Data Centres. AREIT is a great buy, if I have spare cash, I would still buy AREIT for more industrial exposure in Singapore.

Follow Frugal Youth Invests

I hope that you like today’s article. To receive instant notification of any new posts by Mail, you may like to follow my blog which can be found at the bottom of the page.

You can also share this article with your friends, if you find this article useful.

2 thoughts on “Ascendas Reit and Mapletree Industrial Trust Analysis (2020)”